Source : BR

Despite high domestic inflation, supply disruptions due to covid and the recurrence of the virus itself—which has now come back with a vengeance for the third time—businesses in Pakistan are positive about the country’s outlook The cement industry would be a prime evidence of such optimism and in fact may be one of the sectors where such optimism may be originating from in spades.

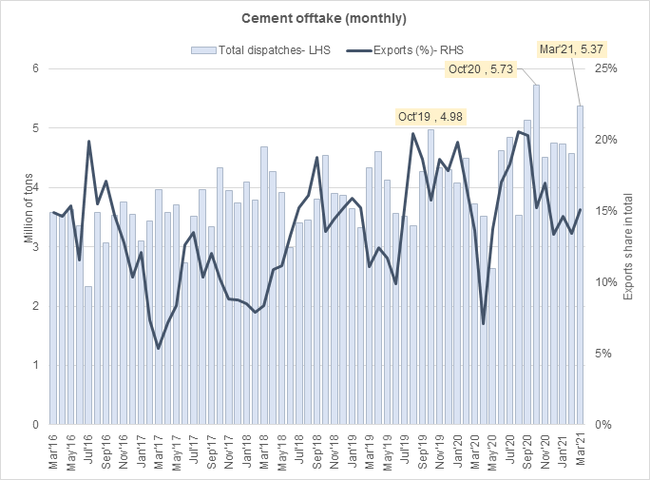

Average monthly offtake over the past nine months is up 17 percent during the current fiscal year compared to the time last year, which granted was expected given that year being a victim of covid onset. But even comparing it to earlier years where annual growth was positive; FY21 continues to shine. For context, average monthly offtake during FY21 so far is up 26 percent, 22 percent and 43 percent compared to FY19, FY18 and FY17 respectively.

It is no surprise that for the year to date (9M), twice the industry has hit the highest sales number in history. First in Oct-20, hitting very close to 6 million tons of cement (of which 75% were domestic dispatches) and the second time last month with exports holding at 15 percent both times. In fact, reliance on exports is slowly waning as domestic markets become ever more attractive on the back of raging demand coming from large construction and hydropower projects. It is a good look on the sector, since domestic markets provide a better margin on sales and where domestic players reign supreme—in export markets, there is a lot of competition that brings down prices.

In fact, the cement industry is now channelling efforts toward targeting (as opposed to merely adjusting sales mix) both domestic and export markets—both of which are growing rapidly. Trade links between India and Pakistan are expecting to be restored soon, while South Africa’s anti-dumping duties on Pakistani cement were also lifted earlier this year. Southern players in the country have also tapped new markets for clinker overseas which are expanding, many due to respective governments’ increasing government spending on infrastructure development.

Meanwhile, local demand prospects are also aplenty on the back of new housing projects under Naya Pakistan Housing (NPHP) where government mark-up subsidies are available for mortgage borrowers. There is also a mandate for banks to at least maintain a 5 percent allocation in private sector financing for the construction sector due to the construction amnesty package announced by the government earlier this year. Though, how much of that 5 percent will actually be utilized towards construction activities is an important question to explore- more on that later.

Nevertheless, NPHP is picking up steam. In just the last month alone, the PM announced an apartment complex project for 2000 people and a laborers’ complex to build 1500 homes in Islamabad. More projects will come specially in Punjab and KP, though hitting snags in Sindh due to a multitude of political reasons.

Projected growth in the cement industry for the upcoming few years has created an expansion opportunity for cement firms, both playing in the top and mid-fields. This opportunity is also further boosted by the SBP’s TERF facility that is providing concessionary financing for businesses that would lower borrowing costs. For the expansions already announced, new capacity may be up by 18 million tons—3-month worth of the current offtake. With the way demand is growing, even that may not be enough